What is Stock Merger Arbitrage?

What is Arbitrage?

In economics, a strategy that takes advantage of a price difference between two or more markets is called arbitrage.

An easy-to-understand example of arbitrage would be in currencies; suppose you have two exchange offices that have the following set of BUY/SELL prices for EUR/USD

![\[\mbox{Office 1} = \left\{ \begin{array}{ll} \mbox{SELL:} & 1.25\\ \mbox{BUY:} & 1.23\end{array} \right. \mbox{Office 2} = \left\{ \begin{array}{ll} \mbox{SELL:} & 1.22\\ \mbox{BUY:} & 1.19 \end{array} \right.\]](https://atypicalquant.net/wp-content/ql-cache/quicklatex.com-2be6d2b258d6a4273a3097d7d4c70f0c_l3.png "Rendered by QuickLaTeX.com")

Under these hypothetical inefficient market conditions, you could secure a guaranteed profit by buying EUR from Office 2 and selling to Office 1.

How can we apply it to stock mergers?

When two companies  and

and  decide to merge, they usually announce a merger rate

decide to merge, they usually announce a merger rate  and a merger time

and a merger time  , usually a few months later.

, usually a few months later.

If at a specific time, the current price rate  is significantly different from , we can create a strategy, based on our assumption that the rate will converge to the merger rate (

is significantly different from , we can create a strategy, based on our assumption that the rate will converge to the merger rate ( ). As long as the merger holds, our strategy will result in a guaranteed profit.

). As long as the merger holds, our strategy will result in a guaranteed profit.

A look at the current APHA / TLRY merger

The maths:

Two Marijuana Stock companies Aphria Inc. (APHA) and Tilray, Inc. (TLRY) have announced a merger at:

![\[\text{APHA}=0.8381 \cdot \text{TLRY}\]](https://atypicalquant.net/wp-content/ql-cache/quicklatex.com-1d0f1864971ab8ec7ffb389fc707ad63_l3.png "Rendered by QuickLaTeX.com")

However, at the time of posting, their ratio is significantly different:

![\[\text{APHA}=0.63 \cdot \text{TLRY}\]](https://atypicalquant.net/wp-content/ql-cache/quicklatex.com-42d916b54e087a221f6533f3d786f405_l3.png "Rendered by QuickLaTeX.com")

We can easily see that APHA is relatively undervalued, but can you set your positions to have a guaranteed return (as long as the merger goes through at the agreed rate)?

Let’s denote with A and T the current prices and with A’ and T’ their converged pre-merger prices. Let’s also call and their current and future ratios.

![\[A = r_0 \cdot T \text{ and } A^{\prime} = r \cdot T ^{\prime} \Longrightarrow \dfrac{A^{\prime}}{A} = \dfrac{T^{\prime}}{T} \cdot \dfrac{r}{r_0}\]](https://atypicalquant.net/wp-content/ql-cache/quicklatex.com-1c1bf36a7106427b94f25ac0bd01a577_l3.png "Rendered by QuickLaTeX.com")

Denoting a, respectively t our dollar amount positions of A and T, our return will be

![\[a\cdot \left( \dfrac{A^{\prime}}{A} - 1 \right) + t \cdot \left( \dfrac{T^{\prime}}{T} - 1 \right) = \dfrac{A^{\prime}}{A} \left( a + t\cdot \dfrac{r_0}{r} \right) - a - t\]](https://atypicalquant.net/wp-content/ql-cache/quicklatex.com-1f79c23cc70099486e9b9cb7a2b9ba0f_l3.png "Rendered by QuickLaTeX.com")

As we want to remove A’s change from our return, we simply select  , which follows in a return of

, which follows in a return of  . As, in our case,

. As, in our case,  , we simply need a negative value of t, and a corresponding positive value of a, and we get a guaranteed profit.

, we simply need a negative value of t, and a corresponding positive value of a, and we get a guaranteed profit.

The strategy (using today’s values):

Given an AUM of x, we set the following positions:

SHORT TLRY:

LONG APHA:

Which will yield a risk-free (except for merger failure) return of:

RETURN:  ( 14%).

( 14%).

Thus, regardless of how far away they drift apart in the meanwhile, and their direction from now, as long as the merger holds at the specified ratio, you will earn a 14% return.

This can be further increased using margin/leverage, after making sure you have a good understanding of your broker’s margin call system / automatic stop-loss.

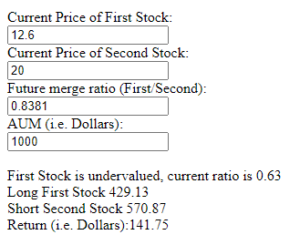

Stock Merger Strategy Calculator:

Use the calculator below to optimize different scenarios:

Due to WordPress limitations, the calculator could not be embedded.

Please use: https://atypicalquant.net/tools/merger_calculator.html