Why is ORA.PA (Orange) my largest holding?

🟩 𝐂𝐨𝐦𝐩𝐚𝐧𝐲 𝐨𝐮𝐭𝐥𝐨𝐨𝐤

- Operates in 27 countries, primarily providing telecom services, but recently also pushing cross-selling in the broadcasting, landline, and internet areas

- Strongly positioned in the European and North African 5G race, currently providing the fastest available network in Romania and France (according to speedtest.net)

- Is well adapted to the changing demographic, with services like Orange YOXO, through its partnership with NFLX (Netflix, Inc) and its acquisition of SecureLink/SecureData

🟩 𝐅𝐢𝐧𝐚𝐧𝐜𝐢𝐚𝐥𝐬 𝐚𝐧𝐝 𝐅𝐮𝐧𝐝𝐚𝐦𝐞𝐧𝐭𝐚𝐥𝐬

- 10.06 P/E ratio ( VOD (Vodafone Group) – 17.86, TMUS(T-Mobile US) – 52.05)

- 0.625 P/S ratio( VOD (Vodafone Group) – 1.094, TMUS(T-Mobile US) – 2.081)

- Significant upside potential in analyst estimates – High dividend yield

🟩 𝐆𝐫𝐨𝐰𝐭𝐡 𝐏𝐫𝐨𝐬𝐩𝐞𝐜𝐭𝐬

- Partnership with NOK (Nokia Oyj) for developing 6G 🚀

- Orange Money, a service offering the convenience of PYPL (PayPal Holdings) or Revolut, but also including various financing options, could drive revenue in the following years

- Can monetize existing infrastructure and assets

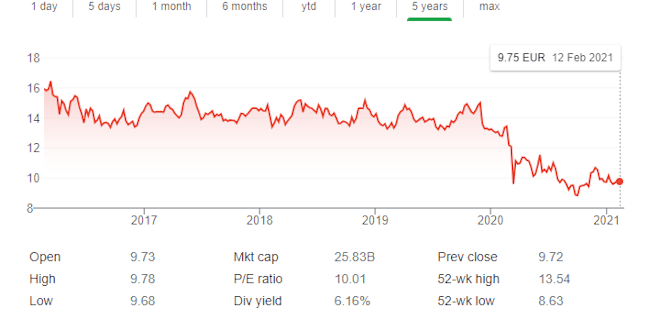

Given all of the above, I expect the stock to at least recover to the 14-16 EUR range in which it stayed consistently in the 2014-2019 timeframe (a 40%+ upside 🚀)

Any thoughts and ideas are welcome in the Latex-enabled comment section below.