Solve the following random variable comparison: what is the probability that X > 4Y if :

1. X, Y independent, standard normally distributed?

2. X, Y independent, uniformly distributed on [0,1]?

Question 1

So, this first part of the question is about two iid standard normal distributions.

Solution 1

We know that if  has a normal distribution,

has a normal distribution,  has as well, with

has as well, with ![\mathbb{E}[cY] = c \mathbb{E}[Y]](https://atypicalquant.net/wp-content/ql-cache/quicklatex.com-4f11a9b0ccf82afe3c68d3078d112193_l3.png "Rendered by QuickLaTeX.com") and

and

The above implies that  .

.

Now, we have both parts of the comparison we want to make.

We can rewrite  as

as  . We also remember the rules pertaining to summing two independent normally distributed random variables and apply them to

. We also remember the rules pertaining to summing two independent normally distributed random variables and apply them to  and

and  .

.

So, we now know that  is a normal distribution, with a mean of 0. Due to the symmetry around the mean of a normal distribution, we conclude that

is a normal distribution, with a mean of 0. Due to the symmetry around the mean of a normal distribution, we conclude that  .

.

Solution 2

With the pair of random variables and (and Y, for that matter) centered around 0, we can split both at the 0 boundaries, marking four quadrants. We employ this partition to extend the probability of  as a sum of conditional probabilities.

as a sum of conditional probabilities.

![\[\mathbb{P} (X > 4Y) = \mathbb{P} (X > 4Y | X \geq 0, Y \geq 0) \cdot \mathbb{P} (X \geq 0, Y \geq 0) \\ + \mathbb{P} (X > 4Y | X < 0, Y < 0) \cdot \mathbb{P} (X < 0, Y < 0) \\ + \mathbb{P} (X > 4Y | X \geq 0, Y < 0) \cdot \mathbb{P} (X \geq 0, Y < 0) \\+ \mathbb{P} (X > 4Y | X < 0, Y \geq 0) \cdot \mathbb{P} (X < 0, Y \geq 0)\]](https://atypicalquant.net/wp-content/ql-cache/quicklatex.com-71464b1400999fcf41ba1a9666b56644_l3.png "Rendered by QuickLaTeX.com")

Given what we said before that X and Y are independent and symmetrical around 0, the probabilities used to weigh the sum are all equal to  .

.

We can also easily see that:

- X is always greater than 4Y when X is positive, Y is negative

- X is never greater than 4Y when X is negative, Y is positive

Replacing all the values derived before, we get a new formula for the probability we are seeking.

![\[\mathbb{P} (X > 4Y) = \dfrac{1}{4} + \dfrac{1}{4}\left( \mathbb{P} (X > 4Y | X \geq 0, Y \geq 0) + \mathbb{P} (X > 4Y | X < 0, Y < 0) \right)\]](https://atypicalquant.net/wp-content/ql-cache/quicklatex.com-19fa0a434109b4298c7f073d78de02a8_l3.png "Rendered by QuickLaTeX.com")

The two probabilities involved on the right-hand side of the equation look very similar, conditioned on opposite quadrants. We can denote  and

and  as the opposites of and and know that they both have the same distribution and are independent, exactly like their counterparts.

as the opposites of and and know that they both have the same distribution and are independent, exactly like their counterparts.

We rewrite the second probability, replacing everywhere X with -X, and Y with -Y, and use the property deduced before to get that the initial value is equal to the probability that X is less than 4Y, conditioned on X and Y greater than 0. Given that they are continuous random variables, we can change the conditioning to X and Y at least 0.

We replace this equivalency in the initial result and use the fact that the two probabilities on the right-hand side are complementary to arrive at the same result as the first solution, 1/2.

Question 2

With two options for the first question under our belt, we can turn our attention to the one involving two independent uniform random variables.

You might jump the gun and say that you get the same result in this case, but it is a false equivalency. The sum of two uniform random variables is not uniform itself. It has an Irwin-Hall distribution. If you knew the probability density function of this, you could use it to find the correct answer to the question. I’d say that the majority doesn’t know this at the top of their heads, so we have to find another solution.

Solution 1

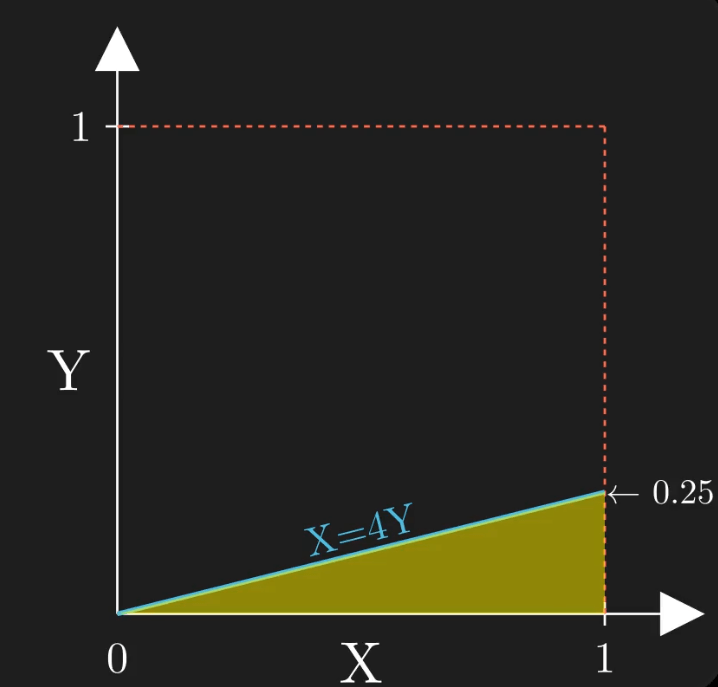

Wanting to visualize the pair of the two random variables uniformly distributed, we get the unit square.

We can draw the line of X=4Y, with the area of the triangle below it representing the space where X is more than 4Y.

Given the distributions and the independence of X and Y, the probability the pair (X, Y) is in this triangle is equal to the area of the triangle scaled by that of the square, which is 1/8.

Solution 2

We can also use convolutions for an analytical solution to this part of the question.

![\[\mathbb{P} (X>4\cdot Y) = \displaystyle\int_0^1\displaystyle\int_0^{\frac{x}{4}} f_Y(y)\text{dy}f_Y(X)\text{dx}\]](https://atypicalquant.net/wp-content/ql-cache/quicklatex.com-19a299680f1a4d37ead5cecd429abe2f_l3.png "Rendered by QuickLaTeX.com")

Since X and Y are uniform, ![f_Y(y) = f_X(x) = id_{[0,1]}](https://atypicalquant.net/wp-content/ql-cache/quicklatex.com-f85834d622b1d554b9880841e14f91d7_l3.png "Rendered by QuickLaTeX.com") .

.

CodingCheck

If the four solutions before were not convincing enough, you can simulate the results and get the same values as those obtained mathematically.

import numpy as np

s = 10**6

## Generate samples for A

x_a = np.random.normal(loc=0, scale=1, size=s)

y_a = 4*np.random.normal(loc=0, scale=1, size=s)

## Generate samples for B

x_b = np.random.uniform(low=0, high=1, size=s)

y_b = 4*np.random.uniform(low=0, high=1, size=s)

## Compute observed probabilities

p_a = '{:.2%}'.format(np.mean(x_a>y_a))

p_b = '{:.2%}'.format(np.mean(x_b>y_b))

## Print results

print(f'Probability (A): {p_a}')

print(f'Probability (B): {p_b}')